The Northwood Group

Building Partner Investors

The Northwood Group

Building Partner Investors

The Election and Commercial Real Estate

As the country went to the polls last week there were many issues influencing how the American people chose to vote. The country’s opinion regarding who would be the best leader of the free world for the next four years was split even among similar demographics with a few exceptions. In the end the voice of the people elected President Obama to be our leader for the next four years.

With the election over, those who voted for Obama and as well as those who voted for Romney are left to wonder what the effect of that decision will be on their individual self interests. How will their lives and industries be affected over the next four years and beyond? The intent of this post is to discuss what effects this election may have on the commercial real estate market in Utah. It is not intended to be an exhaustive document but to touch on some of the ways that the election results may affect us in the commercial real estate industry.

Uncertainty versus Clarity

Many in the commercial real estate industry have looked forward over the past few months to the election with hopes that either result would eliminate much of the uncertainty that has plagued the real estate market this year. Many commercial real estate investors have patiently awaited the outcome as they have planned their acquisitions and dispositions this year. Other investors have disposed of property assets during the second half of the year with growing concerns of increases in capital gains taxes rates in 2013.

Surprisingly, clarity has not returned to the market with the conclusion of the election. The fiscal cliff and questions regarding the President’s economic agenda have left investors pondering. In fact, in my discussions with commercial property investors during the past week some have delayed otherwise active acquisition strategies as they attempt to understand where things are going.

The life-blood of the commercial real estate investment world is the success of the businesses occupying properties and paying rent. Although investment activity in commercial real estate has strengthened during the past year, business growth and occupancy has lagged in several areas. Businesses have been more reluctant to grow than investor’s portfolio’s have. The most common response we hear from companies when asked about their business is that:

What this says is that they have learned to do more with less. Businesses suffered the pain of the initial downturn. They made the difficult decisions regarding cost cutting to stay alive. Now that they are again profitable they are hesitant to re-invest and grow as they did in the past.

This is all without including the effects of health care reform and how it will affect who they hire, how many people they hire and what types of positions they will be opening.

Commercial Real Estate vs. Other Asset Classes

Stock market fluctuations have led many investors out of that market and into the commercial real estate market – many for the first time. There has been a strong demand from individuals and companies wanting to invest in something that they can see, smell and touch. This commercial real estate investment trend should continue until confidence returns to the stock market. Fears of inflation also have led investors back into commercial real estate as it has proved to be a very viable hedge against inflation in past cycles.

Interest Rates

Commercial real estate is more sensitive to interest rates than probably any other economic factor. Many of the deals being transacted across the country could not get done at current pricing if interest rates were to significantly rise. Long-term fixed rate debt becomes increasingly valuable as expectations of a recovery progress.

Taxes

Tax policy, particularly capital gains treatment may be the most significant issue coming out of this election. Is there going to be a capital gains category? If so, where are capital gains tax rates going to be in 2013? 2014? 2015? Those taxes will largely affect the number of real estate sellers coming into the market and limit the number of transactions available for commercial real estate investors.

Conclusion

It will be interesting to see how things progress as 2012 wraps up and we come into 2013. A significant percentage of individuals in the commercial real estate industry tend to lean right and be a little more conservative to differing degrees. Many commercial property investors express real fears of what is perceived to be a negative election result as it relates to the local, national and world economies and more particularly, commercial real estate.

The challenge that those on the right face is not what effect the election will have on the commercial real estate industry but what affect their investment decisions will have on the industry and the economy as a whole. A policy of “doing nothing” even when good opportunities present themselves may create a self-fulfilling prophecy as our fears create the very circumstances we wish to avoid.

With that being said, there are some real challenges and concerns in the economy in coming years and investors should “move” with caution and scrutiny as they always do. The most important verb in that sentence is that they do “move” and make decisions based on objective analysis as opposed to emotional fears.

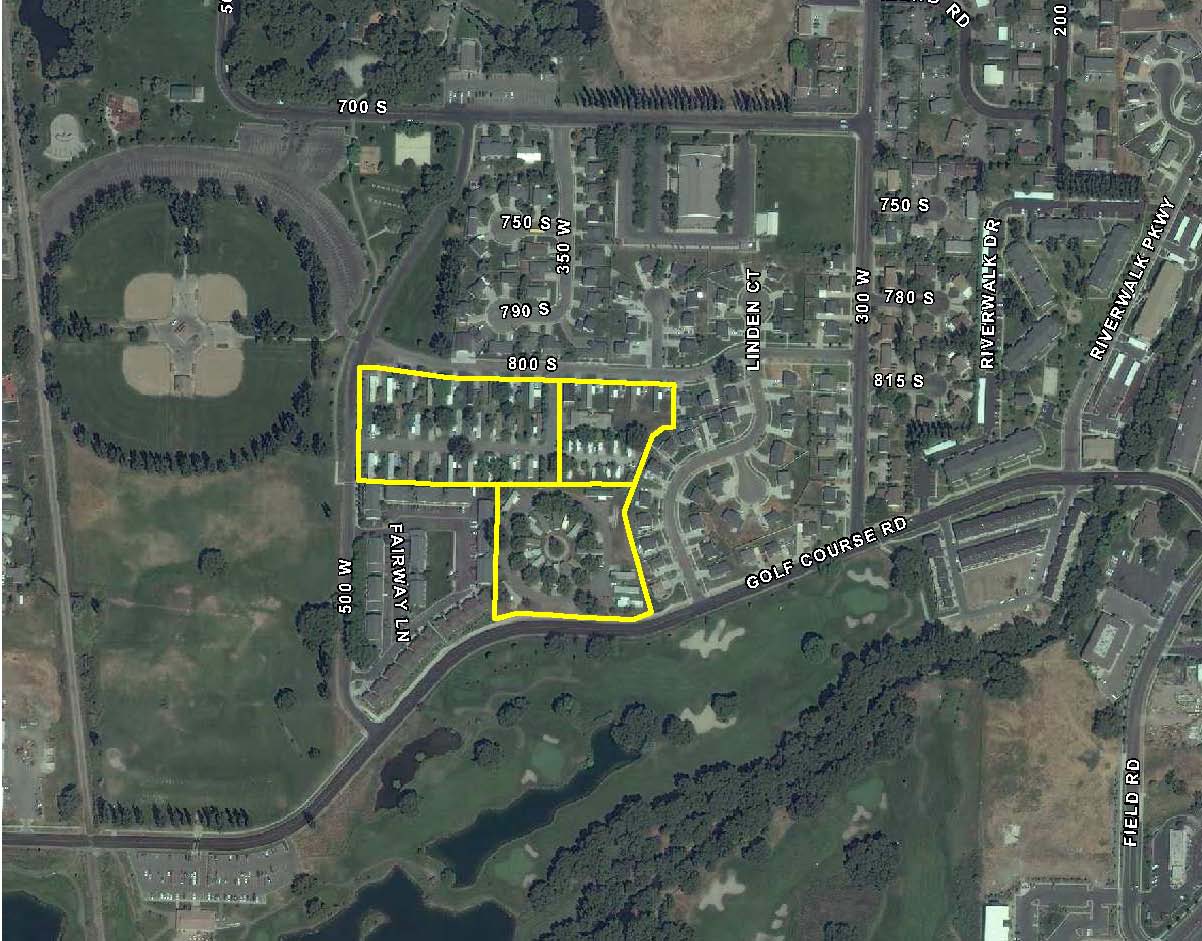

We have recently closed on the sale of the Logan Mobile Home Park in Logan, Utah. The park consisted of a 53 unit mobile home park on 5 acres. It was a unique mobile home park whereas it is situated in a very good area near the local city golf course and baseball fields. The buyer was a local investor and purchased it for cash flow purposes.

We sold another mobile home park investment last month and I included a few thoughts regarding this type of commercial real estate investment. I am including those same comments below:

Several of my clients have been seeking mobile home park investments as an alternative to their typical commercial real estate investments in the last 12 months. Their theory being that because of most cities reluctance to grant zoning for new mobile homes parks, existing parks are experiencing strong occupancies. Unlike most commercial properties, a few vacancies have very little impact on the overall return. It is also a commercial real estate investment type that tends to do better in recessionary economies. The hope is that strong occupancies due to a lack of new supply will provide greater than average rent growth.

The challenge with mobile home park investment is understanding management. There are more nuances dealing with tenants than in traditional properties. Its is also a property type you might not feel proud telling your friends that you own.

If you can get over some of these hurdles there are some real financial advantages. Please feel free to contact me for additional information on the deal points.

We have recently closed on the sale of a mobile home park investment. The Tradewinds Mobile Home Park in Bountiful, Utah was sold to a local investor. The park was an older park consisting of individual, single-wide mobile homes. The purchase included the park only. No homes were included in the sale.

Several of my clients have been seeking mobile home park investments in the last 12 months. Their theory being that because of most cities reluctance to grant zoning for new mobile homes parks, existing parks are experiencing strong occupancies. Unlike most commercial properties, a few vacancies have very little impact on the overall return. It is also a commercial real estate investment type that tends to do better in recessionary economies. The hope is that strong occupancies due to a lack of new supply will provide greater than average rent growth.

The challenge with mobile home park investment is understanding management. There are more nuances dealing with tenants than in traditional properties. Its is also a property type you might not feel proud telling your friends that you own.

If you can get over these hurdles there are some real financial advantages. In addition to this park I have other clients under contract on other parks that we’ll discuss in the future.

We have just completed our analysis for the 3rd quarter of 2012. Please click the link below to see the Q3 Utah Investment Snapshot:

Utah Investment Snapshot – Q3 2012

A few of the highlights from the report are as follows:

Please feel free to contact me with any questions regarding the market information provided.

Please see the following link for the Capital Market Review for the month of October 2012:

Interest rates remain low across the board with the lowest rates in the multi-family sector. The 10-year treasury was up a bit due to the unexpected decline in unemployment. Institutional buyer continue to lead the charge on commercial real estate investment purchasing high-quality assets both in major and more continually secondary markets.

Annual rent increases are a commercial real estate investors best friend. Commercial real estate has long been lauded not only for its strong investment performance but for its hedge against inflation. What other asset can you leverage with fixed rate financing and then have the income increase with time?

When looking at the leases that comprise that income landlords and investors have historically favored fixed rate rental increases. I am defining a fixed rate rental increase as an increase in the rental amount based on a fixed percentage or dollar amount. For example, the rent could increase by 2% annually or 10% every 5 years. Sometimes it is described as a fixed dollar amount as in $500 per year. This rental increase method has been preferred because it is easily definable, calculable, and it simplifies budgeting.

Currently investors face a dilemma when looking at new leases or analyzing commercial real estate investments. There are many economic experts in the country concerned about inflation in coming years. This creates a situation where a fixed rate increase may not keep up with the time value of money creating a situation where the value of the lease actually decreases year to year. Many investors are turning towards rental increases based on inflationary indexes such as the consumer price index (CPI) and other methods. The challenge with this method is that there are many ways to calculate this index and it is difficult to track. It requires an annual discussion with the tenant to determine what rent will be going forward and is sometimes the source of contention and bad feelings if there is a disagreement on how the escalation is being applied.

The flip-side of this coin is that tenants are looking at these same considerations. They don’t want the risk of inflation passed to them either. Strong credit tenants are often times even able to negotiate flat lease rates during their lease terms. In recent years tenants such as Family Dollar and Walgreen’s have become darlings for commercial real estate investors and 1031 exchange buyers. For example, Family Dollar will typically sign 10 year leases during their initial term and will typically require a flat lease rate during that term. Similarly Walgreen’s has been able to obtain leases as long as 25 years with no annual increases. Many investors have concluded that they are willing to take that risk in exchange for the strength of the tenant. What will the value of those rental dollars be at the end of those leases? It is a crystal ball question but if we do experience high degrees of inflation those leases could become problematic.

Regardless of how each individual commercial real estate investors views the threat of an inflationary market, each should be considering this aspect of the investment both in lease negotiations and new property acquisitions.

During the economic downturn, I have had many clients come to me with an interest in taking some of their money out of the securities markets and investing it in raw land. Their theory being that if economic troubles continue, at least they’ll have something they can see, touch, & smell. These are typically individuals who do not own real estate besides their personal residence and often don’t feel like they can or want to understand the management associated with income-producing commercial real estate investments. There are some merits to investing in raw land, but there there are also some challenges associated with it. The intent of this discussion is to lay out the factors that an investor should consider when comparing raw land to income-producing commercial real estate or other financial markets.

POTENTIAL BENEFITS TO INVESTING IN RAW LAND

POTENTIAL CONCERNS TO INVESTING IN RAW LAND

If the decision is made to invest in raw land then there are a number of factors affecting which property to buy. For example, is it in the path of growth? What is the condition of the soils? Where are utilities and services for the property? What will it cost to get them to this property? Do I want agricultural, commercial, residential or other types of property? When will the market allow the property to be developed? Where does the property sit in the city’s master plan? What will ultimately be built on this property? Do I want to develop or sell the property when the time is right? Are there any easements which would adversely affect the property value? Does the property have enough water available for development? These are just a handful of the questions that need to be asked.

If the decision is made to invest in raw land then there are a number of factors affecting which property to buy. For example, is it in the path of growth? What is the condition of the soils? Where are utilities and services for the property? What will it cost to get them to this property? Do I want agricultural, commercial, residential or other types of property? When will the market allow the property to be developed? Where does the property sit in the city’s master plan? What will ultimately be built on this property? Do I want to develop or sell the property when the time is right? Are there any easements which would adversely affect the property value? Does the property have enough water available for development? These are just a handful of the questions that need to be asked.

Under the right scenario’s investing in raw land can be a great investment. I have many clients who focus solely on this type of strategy. I also have many clients who refuse to buy raw land for the reasons listed above but primarily it is because of a lack of cash flow. I have found that as an investor’s net worth increases, his propensity for doing land deals increases.

I hope this is helpful as you assess the place of raw land in your commercial real estate portfolio. Contact me for more information.

I recently read an article that details the potential effects of the LIBOR scandal on Commercial Real Estate Investments. The article was written by David Bodomer of National Real Estate Investor and was a good editorial on the subject. The summary that I took away from it was that the effects on commercial real estate are likely to be minimal unless LIBOR goes away entirely which is unlikely. The biggest effect is more likely to be further uncertainty to the capital markets in a time when we are attempting to recover. The full article is reprinted below.

Sep 12, 2012 11:21 AM, By David Bodamer, Editorial Director

In early July, British investment bank Barclays PLC announced a surprise settlement with agencies from the United States and Europe and admitted that, for years, it had been reporting false information to the British Bankers’ Association as part of the process of determining the London Inter Bank Overnight Rate (LIBOR)—a key metric used as the basis for trillions of dollars’ worth of other financial products, including some commercial real estate debt. The bank agreed to pay more than $450 million in fines: $200 million to the U.S. Commodity Futures Trading Commission, $160 million to the criminal division of the U.S. Department of Justice and $92.8 million to Britain’s Financial Services Authority.As a result of the scandal, key executives—including Barclays Chairman Marcus Agius and Barclays CEO Robert Diamond—announced their resignations. The bank is now fighting to regain the trust of investors, borrowers, other banks and regulatory agencies in the wake of the revelations.And, allegedly, it wasn’t alone. More than a dozen other banks remain under investigation by European and U.S. financial regulatory bodies for doing the same thing as Barclays. More fines may be handed down. And they are likely to be heftier than what Barclays paid since agencies went easy on the British bank for being the first institution to step forward and admit to wrongdoing.The scandal has also triggered dozens of lawsuits as community banks, borrowers, investors and municipalities affected by LIBOR try to recoup potential losses that resulted from inaccuracies in the reported rates. For example, entities including Charles Schwab and the City of Baltimore filed suits against the banks that submit LIBOR rates accusing them of price fixing, under the Sherman Antitrust Act.The docket has gotten so full, in fact, that U.S. District Judge Naomi Reice Buchwald in early August suspended several new lawsuits until the outcomes of the many lawsuits in progress had been determined.Overall, it is estimated that up to $800 trillion in loans, swap arrangements, derivatives and other financial contracts are based on LIBOR. So changes in the rate—as well as its manipulation—have massive potential knock-on effects for a wide variety of institutions.The scandal has died down some since the initial firestorm early this summer. But it threatens to flare back up, depending on the results of the investigations and negotiations still taking place.There were two phases to Barclays’ duplicity. Barclays admitted to reporting the rate higher prior to 2008 in order to improve its position on some derivatives contracts. In this phase, it’s possible that borrowers that placed loans on LIBOR were paying higher interest rates than what should have been available while lenders benefited.Barclays admitted to reporting lower rates after the financial crisis. This primarily would have benefited borrowers and hurt smaller lenders that looked to LIBOR as the benchmark on which to base interest rates.There are direct implications for the commercial real estate sector.LIBOR is commonly used to set the rates for construction loans, floating rate bridge loans and two-, three- and five-year mini-perm loans. Loans are priced at a spread to LIBOR itself.So manipulation of LIBOR means that loans done during the past decade may have been mispriced, depending on the extent that LIBOR was distorted. Barclays alone couldn’t have shifted the rate that much. But if more banks were doing the same thing, rates may have been off significantly.LIBOR was also used by conduit lenders for floating rate loans. This largely affects legacy issues since overall CMBS issuance remains low today. But here too borrowers probably benefited. If anyone got cheated it was investors at the back end that may have gotten lower returns on their investment than if LIBOR had not been manipulated.

Still, analysts don’t believe the CMBS sector has been affected that greatly by the situation.

“‘The current LIBOR controversy does not effect CMBS defaults, losses or ratings, given significant interest rate stresses assumed in our analysis. Plus only a small portion of CMBS are floaters,” says Dan Chambers, managing director with rating agency Fitch.

Borrowers have “enjoyed record low, dirt cheap rates,” says Mark Scott, founder and principal of Commercial Mortgage Capital Corp. “But you have to believe that lenders are going to be upset regarding the fact that they were undercharging customers. They could have been getting a greater yield had LIBOR not been manipulated.”

What happens next is anyone’s guess. In the worst case scenario—LIBOR being scuppered entirely—existing loans and new loans would have to be set to a new index. That process could be drawn out and at least temporarily slow the volume of lending until new standards are agreed upon.

To date, however, the worst case appears unlikely. Banks and borrowers have shown no desire to shift away from LIBOR. And while there have been calls to reform how the number is determined to add greater transparency to the process, there are few, for now, calling for it to be eliminated entirely.

In the commercial real estate sector, lenders continue to originate construction and bridge loans based on LIBOR and volume has not been affected since the scandal broke out.

For example, in late August, Prime Group Realty Trust refinanced its 330 North Wabash Avenue property in Chicago with the proceeds of a $200 million first mortgage loan from Landesbank Hessen-Thuringen Girozentrale and New York Life Insurance Co. The loan consists of a $111.9 million initial advance to repay the existing first mortgage loan on the property and $88.1 million in subsequent advances for tenant and capital improvements. The interest rate on the loan is 30-day LIBOR plus 2.85 percent.

At the heart of the issue is the way LIBOR is determined. The rate is set by a panel of 18 banks that report daily estimates of what interest rate they think they would need to pay to borrow money for three months from other banks. The top four and bottom four estimates are discarded, and that day’s LIBOR rate is the average of the remaining 10 rates.

However, the numbers aren’t based on actual transactions—they’re estimates. So there’s no way to check their accuracy. In fact, the money center banks have largely stopped borrowing from each other since 2008. Instead, they do most of their interbank borrowing directly from central banks where interest rates close to 0 percent remain available. What that means is that LIBOR has become a theoretical measure rather than an index of actual market activity.

Moreover, banks have a massive incentive to lie about what the rates are for various reasons.

According to the British news magazine The Economist, “[E]ven relatively small moves in the final value of LIBOR could have resulted in daily profits or losses worth millions of dollars [on these investments]. In 2007, for instance, the loss (or gain) that Barclays stood to make from normal moves in interest rates over any given day was £20 million ($40 million at the time).”

In the wake of the financial crisis LIBOR took on another meaning: it became a proxy for the health of the major financial institutions. Those reporting higher LIBOR rates were seen as weaker. Therefore, banks had an incentive to report lower rates to signal to investors that they remained solvent and stable.

Richard K. Green, director of the University of Southern California Lusk Center for Real Estate, has been attempting to create a model to determine whether banks would be more likely to over- or underreport LIBOR given different market conditions.

The overall premise is that every bank would lie in order to improve their position. But because banks, depending on different scenarios, could find it fortuitous to report both higher and lower rates, it’s difficult to determine exactly how LIBOR is likely to be distorted.

“The outcome of gaming is not at all clear,” Green says. “Weak banks have an incentive to say a low number, so they can borrow at low rates. Strong banks have an incentive to say a high number, so they can lend at higher values.”

Green plans to continue to develop the model and try to determine how the gaming of LIBOR ultimately affects borrowers, including commercial real estate investors.

What has happened

So far, the commercial real estate sector seems immune from any potential deleterious effects of the LIBOR scandal.

Commercial and multifamily mortgage origination volumes during the second quarter of 2012 were up 25 percent from second quarter 2011 levels, and up 39 percent from the first quarter of 2012, according to the Mortgage Bankers Association’s (MBA) Quarterly Survey of Commercial/Multifamily Mortgage Bankers Originations. Anecdotally, lenders and intermediaries are reporting that activity has remained healthy throughout the summer, even after the news about LIBOR broke.

The MBA index does not include construction loans. But indications are that originations have not slowed in that area of the market either.

“We have not seen a slowdown in the momentum in construction lending,” says Sam Chandan, president and chief economist of real estate and economics analysis firm Chandan Economics. The firm tracks loan volumes and activity nationwide.

Moreover, some experts argue that even if LIBOR was distorted the effects were likely too small to have hurt borrowers dramatically.

“It seems minimal in how it may impact commercial real estate and quite frankly, it’s unquantifiable,” says William E. Hughes, a senior vice president and managing director of Marcus & Millichap Capital Corp. “You get an interest rate, you’re floating it 300 over LIBOR, but the fact of the matter is there is little impact if LIBOR was a few basis points higher or lower than it should have been. … I’m not sure you can effectively quantify the impact in a transaction unless it’s an ultra-large transaction or ultra-large client.”

But it may not have affected borrowers at all, Hughes argues.

“If banks conspired to increase LIBOR, correspondingly, they could have been adjusting spreads down. Or if rates were down, spreads may have been up. So the all-in rate may not have been affected at all,” he says.

One sign that the sector has not sweated the LIBOR situation that much is the fact that it seems no commercial real estate firms are involved in the myriad lawsuits that have been launched in recent months. None of the sources interviewed for this article could name an example of a commercial real estate borrower joining a potential class action lawsuit.

The implications

Part of what’s at play is that borrowers in the commercial real estate sector don’t look that deeply into how LIBOR is determined. They engage the measure more passively.

“We line up at the pump and pay the price there and shop around for the best deal,” says Jeffrey Weidell, president of Northmarq Capital LLC, a financial intermediary. “The cynic in me says LIBOR is like a sausage. Nobody wants to know how it gets made. … It is probably always manipulated. But as long as the rate is low, borrowers are ultimately satisfied.”

That means the biggest challenges for the commercial real estate sector would only emerge if LIBOR ceases to exist. At this stage, that seems unlikely. Replacing LIBOR would be extremely disruptive because of the number of derivatives contracts that would have to be rewritten. The financial industry would like to avoid this. Instead, the United Kingdom’s Financial Services Authority is developing recommendations for how to overhaul LIBOR to make it more transparent and allow it to retain its position as a major benchmark for other interest rates. The authority has issued a 58-page paper outlining some potential reforms and discussions are expected to continue throughout the fall on the potential changes.

Still, if LIBOR were to be dumped, there are several scenarios in how it could be replaced.

One idea that’s being floated is a hybrid system in which banks would continue to give estimates of their borrowing costs, but also mandate that the numbers include some documentation as to how the estimate was reached or examples of actual transactions.

“I think it’s not going to shake things up, unless there’s some massive overhaul and the elimination of LIBOR,” says David Pascale, senior vice president with George Smith Partners, a real estate investment banking firm. “The market would become volatile unless it was telegraphed well in advance and it was orderly.”

Many loan documents do outline specific conditions of what happens if LIBOR ceases to exist, says Scott. The rate will be reset according to a rate based on U.S. Treasuries reported two days prior to the rate lock.

However, other documents are more vague on what will happen if LIBOR is discontinued.

“In some documents, it says if LIBOR goes away that we will come up with a new index. But it doesn’t say how,” Weidell says. “If that happens, there will be scrambling.”

The replacement index for LIBOR doesn’t necessarily need to be in the same interest rate range as LIBOR itself. After briefly spiking in late 2008 and early 2009, one-month LIBOR has generally been less than 0.30 percent since. Three-month LIBOR has been about 20 basis points greater and six-month LIBOR has been about 50 basis points greater.

The replacement index could be a higher base. But the spread could be tightened. That would leave the all-in rates for borrowers on loans virtually the same as they are.

Two likely possibilities are that the finance sector would turn either to short-dated Treasuries or the corporate bond market. “The likelihood that we’d see the reliance on a benchmark that is more esoteric than that is very low right now,” Chandan says.

Another possibility would be the prime lending rate, which runs approximately 300 basis points above the federal funds rate determined by the Federal Reserve Bank.

However, such a shift may not be as disruptive as it sounds.

“The use of LIBOR as a benchmark is in part a reflection of the indices being fairly well embedded,” Chandan says. “But that doesn’t mean we haven’t developed alternative benchmarks that are more transparent and calculated in a way that is market based.”

Ultimately, the most serious outcome of the LIBOR situation may not be the direct effects. Instead, the problem is that it adds further uncertainty to capital markets that still have not fully recovered from the 2008 financial crisis.

“It’s more anxiety and uncertainty in a market that has very slowly been trying to find its footing,” Scott says. “The commercial real estate lending market has been soft over the past three years. … It’s just starting to feel its way out of the dark. This isn’t earth shattering, but it is a cause for pause.”

Further development of the LIBOR scandal could shake up capital markets because of the sheer volume of financial products it affects. The sorting out of trillions in derivatives contracts, for example, could eat up time and resources and end up slowing the pace of lending again.

“It would cause investors to be risk averse and be bad for credit markets,” Pascale says.

Another cause for concern is that the LIBOR scandal is another black eye for the financial services industry, which could increase the calls for further regulation. That, in turn, may have unintended consequences for the commercial real estate sector by making capital more expensive and harder to come by.

“We have all this talk of more control, more government intervention, more oversight and that could lead to more restriction and less of an open market world in which we live,” Hughes says. “I think therein lies the biggest potential risk.”

One of the great challenges when buying commercial real estate today is understandingthe size of the building that you’re buying. There are so many different ways to measure a building that it makes it difficult to compare buildings accurately.

There are many property owners throughout the country that will measure their properties according to BOMA (Building Owners and Managers Association) standards. This organization has attempted to come up with standards for measurement of different property types that can be universal among markets. Unfortunately, property owners are not required to abide by these standards. Many national tenants will require in their leases that the building be measured according to these standards which can help to bridge the gap. The link to the BOMA Standards is http://www.boma.org/standards/Pages/default.aspx

So how do most investors analyze square footage? Most will rely very heavily on the rent roll and the existing leases. The logic being that if two parties who are financially incentivized to come up with the correct square footage have agreed on a particular square footage number, then it likely will be correct. They will then back that up with the appraisal. However, there is no assurance that the appraiser is not relying on the rent roll and leases as well. There is also the differences in property types. The square footage is much easier to identify in a small single-tenant retail deal than it is a 30 story, multi-tenant office building with lobbies, hallways and fitness areas to appropriate to all of the tenants.

What then should an investor do? I don’t know that there is a correct answer for every investment. Should an investor hire an architect during the due diligence process to verify for themselves? I have rarely seen this in practice although that is one possible solution. I think that a proper understanding of the potential pitfalls is sufficient for most investors so that potential discrepancies can be identified early on and the decision can be made on how much due diligence to do on this particular issue.

It is interesting to look at how interest rates have moved over the last couple of months. Across the board rates have continued to drop since May. Additional lenders have continued to come back into the market. Underwriting remains strict but there are more sources of financing re-entering the market weekly.

One note in the report that caught my attention was the Fitch Ratings which project that $24 billion of US CMBS loans are set to mature over the next 12 months and of these loans 41% would be unable to refinance (without additional cash) based on Fitch’s defined stressed refinance parameter (DSCR of 1.25, rate of 8% amortized over 30 years).

It will be important to watch over the coming year how many of these loans default and how many are able to be refinanced.

Please see the following link for the Capital Market Review for the month of August 2012: